[Policy paper]

Grounding solar ambitions

[ Date Published ]

10 June 2026

[ Focus area ]

Sustainability

[ Title ]

Grounding solar ambitions

Land use implications and planning strategies for large-scale solar expansion in Peninsular Malaysia

[ Foreword ]

Malaysia’s energy transition is unfolding in real time, scrambling to meet the country’s commitment to achieving net zero emissions by 2050. Alongside this is the pressing need to strengthen energy security and support economic growth, all of which will require a significant expansion of renewable energy infrastructure over the coming decades. Solar power is expected to sit at the centre of this transition.

At first glance, the proposition appears straightforward. Malaysia possesses considerable solar potential, receives strong year-round sunlight and has increasingly positioned renewable energy as a pillar of national development planning. Yet beneath this optimism lies a more difficult question, one that this paper confronts directly: where will all of this infrastructure actually go?

Challenges with large-scale solar deployment is often discussed through the lens of the cost associated with the photovoltaic panels itself, overlooking the fact where land is among the most finite and contested of resources. The same spaces identified for future solar deployment may also be needed for housing, industrial expansion, transport infrastructure, agriculture, and environmental conservation. As Malaysia’s electricity demand accelerates – driven in part by the rapid growth of energy-intensive sectors such as data centres – these pressures will only become more pronounced.

The challenge herein does not simply involve physical space and the lack thereof. Geographical and spatial realities such as terrain conditions, flood risks, ecological sensitivities and proximity to existing grid infrastructure all shape whether a site can realistically support large-scale solar development. Muddying the waters and adding a further layer of complication are the attendant complexities of land governance – where differing state-level priorities and approval processes can complicate federal-level energy planning objectives.

None of this, however, diminishes the importance of renewable energy expansion. Rather, it underscores the need for greater realism and strategic coordination in how the transition is approached. Calling for the large-scale deployment of solar energy is easy but unpacking its implementation vis-à-vis spatial and governance constraints may be a different story altogether.

It is in this context that the paper was written. Its intention is not to argue against solar development, but to encourage a more grounded conversation about how Malaysia can pursue decarbonisation while managing the competing demands placed upon its land, infrastructure and long-term development priorities.

Datuk Prof Dr Mohd Faiz Abdullah

Executive Chairman

[ Executive Summary ]

- Malaysia has formalised its commitment to achieving net-zero greenhouse gas emissions by 2050 through the Twelfth Malaysia Plan and the National Energy Transition Roadmap (NETR). To meet the target of 70% renewable energy capacity, solar power is projected to contribute approximately 58% of the national generation mix. While Peninsular Malaysia possesses a vast technical solar potential of 269 GW, the transition from roadmap to reality introduces a critical land-energy nexus challenge.

- This land use challenge is further intensified by an unprecedented surge in electricity demand, driven by Malaysia’s rapid emergence as a premier regional data centre hub. With cumulative live capacity expanding at a compound annual growth rate of 55.6% since 2019, data centres have become a dominant driver of new energy requirements. Since these facilities are exceptionally electricity-intensive, analysis suggests that incorporating this data centre growth could push future installed capacity requirements to nearly twice the levels projected under the NETR-aligned demand scenario.

- Results from the Regional Sustainable Energy Transition Planning model indicate that meeting the electricity demand under a Data Centre Expansion scenario would require approximately 1,500 km² of cumulative land for solar development by 2050. This requirement corresponds to 82% of the total bare land currently identified in Peninsular Malaysia. This poses a significant strategic challenge, as the same land is vital for future housing, industrial expansion and infrastructure. Furthermore, a geographical mismatch exists between data centres and the suitable land available for large-scale solar deployment.

- The amount of land realistically deployable for solar development is substantially smaller than the amount of undeveloped land that may appear available from a purely spatial perspective. Technical viability is limited by the need for flat terrain and proximity to existing grid infrastructure; remote or fragmented sites often require prohibitive additional investment. Furthermore, climate-related risks, particularly flooding, which accounts for 85% of Malaysia’s natural disasters, and ecological concerns, such as human-wildlife conflict, further reduce the pool of viable development sites.

- Even when technically suitable land is identified, the mobilisation process remains administratively complex because land administration and development approvals remain under state jurisdiction. This results in considerable variation in regulations, land title conversion requirements and approval procedures across different states. The varied governance structure reflects a potential disconnect between national renewable energy ambitions and state-level economic priorities. Decisions regarding land allocation are often influenced by local industrial or tourism targets, meaning that technically suitable land may not be prioritised for renewable energy development under existing local planning frameworks.

- Malaysia must adopt four strategic recommendations. First, retired solar photovoltaic sites should be “repowered” by upgrading ageing facilities with modern technology to reuse established land and grid infrastructure. Second, land use efficiency should be enhanced through technological innovation by rewarding high-yield solar modules in future procurement rounds. Third, floating solar development should be scaled up by utilising water bodies, such as reservoirs and ex-mining lakes, through integrated spatial planning. Finally, dual-land use and agrivoltaic systems should be promoted by allowing solar generation and agricultural production to coexist, ensuring that energy expansion does not compromise national food security or local livelihoods.

[ 1. Introduction ]

Malaysia has committed to achieving net-zero greenhouse gas emissions by 2050, a target formalised in the Twelfth Malaysia Plan.1 Since then, the country has progressively strengthened its renewable energy and decarbonisation agenda through major national policy frameworks, including the Malaysia Renewable Energy Roadmap (MyRER),2 the National Energy Policy 2022–20403 and the National Energy Transition Roadmap (NETR).4 Under the NETR, Malaysia targets 70% renewable energy capacity by 2050, with solar energy projected to contribute approximately 58% of that total installed capacity.5 These developments reflect a strong national commitment towards accelerating low-carbon electricity generation.

According to the Sustainable Energy Development Authority in its MyRER portal, Peninsular Malaysia possesses substantial solar energy potential at approximately 269 GW, supported by favourable solar irradiation throughout the year.6 However, transitioning from this technical potential into actual large-scale deployment necessitates addressing significant spatial and land use implications, particularly for ground-mounted solar systems that require extensive land areas.

These land use challenges are intensifying, alongside the rising electricity demand in Peninsular Malaysia. Such a trend has been accelerated by the country’s rapid data centre development. As one of the fastest-growing data centre markets in Southeast Asia, Malaysia has seen the cumulative live capacity of data centres expand rapidly since 2019.7,8 As data centres are highly electricity-intensive and operate continuously, their growth directly dictates the scale of renewable energy deployment required. Given that solar power is projected to remain as the dominant source of future renewable capacity additions under the NETR, when additional electricity demand from accelerated data centre growth is incorporated, land use pressure is expected to intensify further, increasing competition with industrial development, agriculture, housing, environmental conservation and other strategic land uses.9 The challenge is further exacerbated by the geographical mismatch between major electricity demand centres and land availability.

Consequently, future solar energy expansion can no longer be assessed solely from an electricity generation perspective but must also account for spatial limitations and land use competition. This policy paper presents an evaluation of land use implications of large-scale solar deployment under two future electricity demand scenarios for Peninsular Malaysia: (i) an NETR-aligned demand scenario and (ii) a data centre expansion scenario, which accounts for additional electricity demand growth from the digital economy.

Specifically, this policy brief examined the following:

- The scale of future solar capacity expansion required under both scenarios

- The corresponding land requirements associated with large-scale solar deployment under both scenarios

- Land use challenges associated with large-scale solar development

- Potential strategies to reduce land use pressure and improve land use efficiency

The findings are translated into actionable policy recommendations aimed at supporting Peninsular Malaysia’s long-term energy transition, while balancing renewable energy expansion, land use sustainability and future economic development needs.

[ 2. Solar expansion and emerging demand pressures in Peninsular Malaysia ]

Malaysia’s solar policy landscape has evolved significantly over the past decade, transitioning from an early-stage support mechanism into a more competitive and market-oriented ecosystem aligned with the country’s broader energy transition agenda. This evolution provides a strong foundation for future solar capacity expansion under the country’s energy transition pathway. Yet, emerging demand pressures coming from rapid data centre growth are prompting greater adoption of solar power. The following subsections present an outline of the evolution of solar capacity expansion and an examination of how new demand centres are reshaping Peninsular Malaysia’s electricity needs.

2.1 Evolution of solar market development in Peninsular Malaysia

The evolution of Peninsular Malaysia’s solar market development can be broadly categorised into three key phases: Phase 1: initial market seeding to reduce investment risks and stimulate early adoption; Phase 2: competitive scaling through utility-scale and distributed solar programmes; and Phase 3: aligning solar development with net-zero ambitions through long-term roadmaps, market liberalisation, and market-based procurement frameworks. Each phase and its associated policy instruments are discussed in detail.

Phase 1: Market seeding (2011–2015)

Malaysia’s early solar deployment efforts were anchored by the introduction of the Feed-in Tariff mechanism under the Renewable Energy Act 2011.10 This mechanism played a foundational role in developing Malaysia’s domestic solar industry by reducing investment risks and establishing early technical and institutional capabilities to stimulate early market participation. At a time when solar photovoltaic (PV) technologies were relatively costly, the Feed-in Tariff provided guaranteed premium tariff rates for renewable electricity supplied to the grid. Following this, as global solar costs declined, policy focus shifted towards more competitive and market-oriented procurement instruments.

Phase 2: Competitive scaling (2016–2020)

The second phase marked a transition towards scaling solar deployment through competitive and market-based mechanisms. Since 2016, various programmes, such as the Large-Scale Solar (LSS) programme,11 the Net Energy Metering (NEM) programme12 and the Self-Consumption scheme,13 have formed the backbone of solar deployment in Peninsular Malaysia. The LSS programme is a government-led initiative designed to support large-scale solar power deployment in Peninsular Malaysia through a structured competitive bidding process managed by the Energy Commission.14 Since the first round of LSS bidding in 2016, the LSS bidding quotas have increased from 354 MW in LSS1 to approximately 2 GW in the most recent LSS5+ in 2025.15 This has provided a structured pipeline for large-scale solar capacity, contributing significantly to 6,028 MW of solar capacity growth in Peninsular Malaysia.16

In parallel, distributed solar adoption has been supported through the NEM scheme. Executed by the Ministry of Energy and Natural Resources and regulated by the Energy Commission, with the Sustainable Energy Development Authority Malaysia as the implementing agency, NEM 1.0 allowed consumers to install rooftop solar for self-consumption, and excess electricity can be exported to the grid to offset electricity bills at displaced costs.17 While initial uptake under NEM 1.0 was limited, reforms under NEM 2.0 in 2019 introduced a one-to-one offset mechanism, allowing excess electricity to be offset at retail tariff rates. This significantly improved the financial attractiveness of rooftop solar installations. This momentum continued after NEM 3.0 was introduced in 2020, which expanded quota allocations from 500 MW to 1,950 MW and introduced more targeted structures for different consumer segments, including the NEM Rakyat programme, the NEM GoMEn (Government Ministries and Entities) programme and the NOVA (Net Offset Virtual Aggregation) programme.18

Complementary mechanisms, such as the Self-Consumption scheme, introduced in 2017, allow households to generate and use electricity from self-installed solar PV systems to offset electricity bills. In addition, the solar leasing scheme introduced in 2019 under the Supply Agreement for Renewable Energy (SARE) expanded access to rooftop solar through third-party ownership and solar leasing arrangements. By reducing upfront investment barriers, SARE accelerated commercial and industrial rooftop solar adoption, while enabling broader private sector participation.

Phase 3: Net-zero alignment with market liberalisation (2021–present)

Following earlier developments, Peninsular Malaysia’s solar adoption initiatives direction has increasingly evolved beyond renewable energy promotion towards broader decarbonisation and market transformation objectives. In 2021, MyRER was introduced, which established a more coordinated long-term strategy for scaling renewable energy deployment across the country. The roadmap targets renewable energy to contribute 31% of national installed capacity by 2025 and 40% by 2035.19 Solar energy was identified as a key driver of this transition, supported by assessments indicating substantial deployment potential across Peninsular Malaysia, including approximately 94.9 GW of ground-mounted solar potential, 37.4 GW of floating solar potential and 5.2 GW of rooftop solar potential.

This policy direction was further reinforced through the launch of the NETR in 2023, which positions solar power as a central pillar of Malaysia’s long-term energy transition pathway.20 Under the NETR, solar is projected to contribute approximately 58% of total installed capacity in support of the national target of achieving 70% renewable energy capacity by 2050.

Parallel to these strategic roadmaps, Malaysia introduced several market liberalisation mechanisms aimed at expanding corporate and community adoption of renewable electricity. In 2022, the Corporate Green Power Programme (CGPP) was introduced to enable corporate consumers to participate in a virtual power purchase agreement (VPPA) with solar developers. Under this programme, corporate consumers can procure renewable energy attributes and sustainability benefits from dedicated renewable energy developers.21 This helps corporations meet sustainability commitments and offset electricity consumption beyond their own on-site generation. Building on this, the Corporate Renewable Energy Supply Scheme (CRESS) was later introduced in 2024 as a more liberalised successor to CGPP.22 Unlike the VPPA-based structure under CGPP, CRESS enables corporate consumers to directly purchase green electricity from renewable energy developers through the national grid under the Third-Party Access framework guided by the New Enhanced Dispatch Arrangement. In parallel, market-based instruments, such as the Renewable Energy Certificate framework introduced in the same year, have enabled corporate consumers to procure and attribute renewable electricity towards sustainability commitments. These developments signify an important transition from centrally allocated renewable energy quotas towards more liberalised market-based procurement structures.

At the community level, the Malaysian government introduced the Solar for Rakyat Incentive Scheme in 2024, providing rebates for residential rooftop solar installations under the NEM framework.23 To promote residential solar adoption, the Community Renewable Energy Aggregation Mechanism, launched in 2025, enables local consumers to access solar electricity from nearby rooftop systems through the distribution network.24 In the recent call of NEM 3.0, the quota allocations have also been expanded from 450 MW to 700 MW for the NEM Rakyat programme and from 1,400 MW to 1,700 MW for the NOVA programme.25 Recent reforms have also shifted distributed solar policies towards a stronger emphasis on self-consumption by replacing NEM 3.0 with the Solar Accelerated Transition Action Programme.26 This programme allows the transition from one-to-one export credit arrangements towards compensation based on the system marginal price.

Collectively, these developments demonstrate that Malaysia has established a rising ecosystem that supports both large-scale ground-mounted solar and distributed rooftop solar deployment across utility-scale, commercial, industrial and residential sectors. As summarised in Fig. 1, the evolution of these initiatives reflects the progressive expansion of renewable energy programmes, procurement pathways and private sector participation over time, indicating growing policy commitment and market readiness to accelerate the region’s solar adoption.

2.2 Emerging demand pressures from rapid data centre growth

While Peninsular Malaysia has established increasingly supportive solar policies and market mechanisms over the past decades, maintaining a reliable electricity supply under rapidly growing demand is emerging as a critical challenge for the power sector. Prior to the recent acceleration in data centre investments, Peninsular Malaysia is projected to require an additional 14 to 15 GW of generation capacity by 2030 to support rising domestic electricity demand.27 However, the rapid emergence of Malaysia as a regional data centre hub is now significantly altering this outlook.

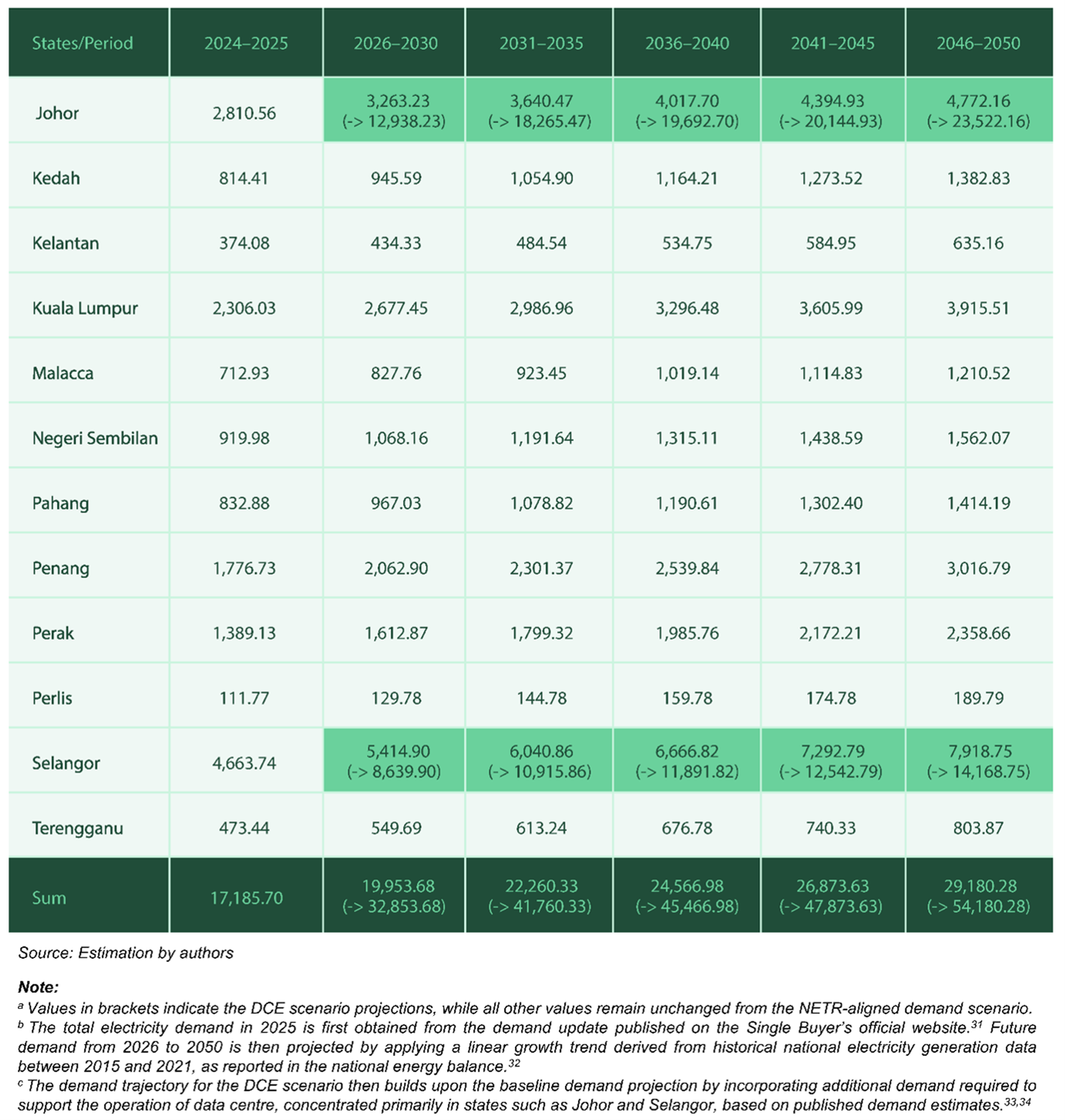

Malaysia currently represents one of the largest concentrations of proposed data centre developments in Southeast Asia, accounting for approximately 3.4 GW, or nearly 60%, of total projects proposed in 2026.28 Since 2019, the cumulative live data centre capacity has expanded at a compound annual growth rate of 55.6%, with major investments concentrated in Johor and Greater Kuala Lumpur.29 To meet corporate decarbonisation targets and carbon usage effectiveness standards, many technology companies operating data centres have committed to sourcing electricity from renewable energy. Carbon usage effectiveness measures the total carbon emissions per total energy generated, which differs based on the source of energy and quantity consumed.30 Nevertheless, as these facilities are highly electricity-intensive and operate continuously, their expansion is expected to drive a massive increase in renewable energy demand, particularly for solar, in power systems. In Table 1, the projected electricity demand, based on the published estimated additional demand required to support the operation of data centres, is summarised.

Fig. 1. Summary of evolution of solar policy and market mechanism in Peninsular Malaysia

Table 1. Estimated electricity demands under NETR and DCE scenarios

Source: Estimation by authors

Note: The values in brackets indicate DCE scenario projections, while all other values remain unchanged from the NETR-aligned demand scenario. The total electricity demand in 2025 was first obtained from the demand update published on the Single Buyer’s official website.31 Future demand from 2026 to 2050 was then projected by applying a linear growth trend derived from historical national electricity generation data between 2015 and 2021, as reported in the national energy balance.32 The demand trajectory for the DCE scenario then builds upon the baseline demand projection by incorporating additional demand required to support the operation of data centres, concentrated primarily in various states, such as Johor and Selangor, based on published demand estimates. 33,34

[ 3. Current landscape of land use in Peninsular Malaysia ]

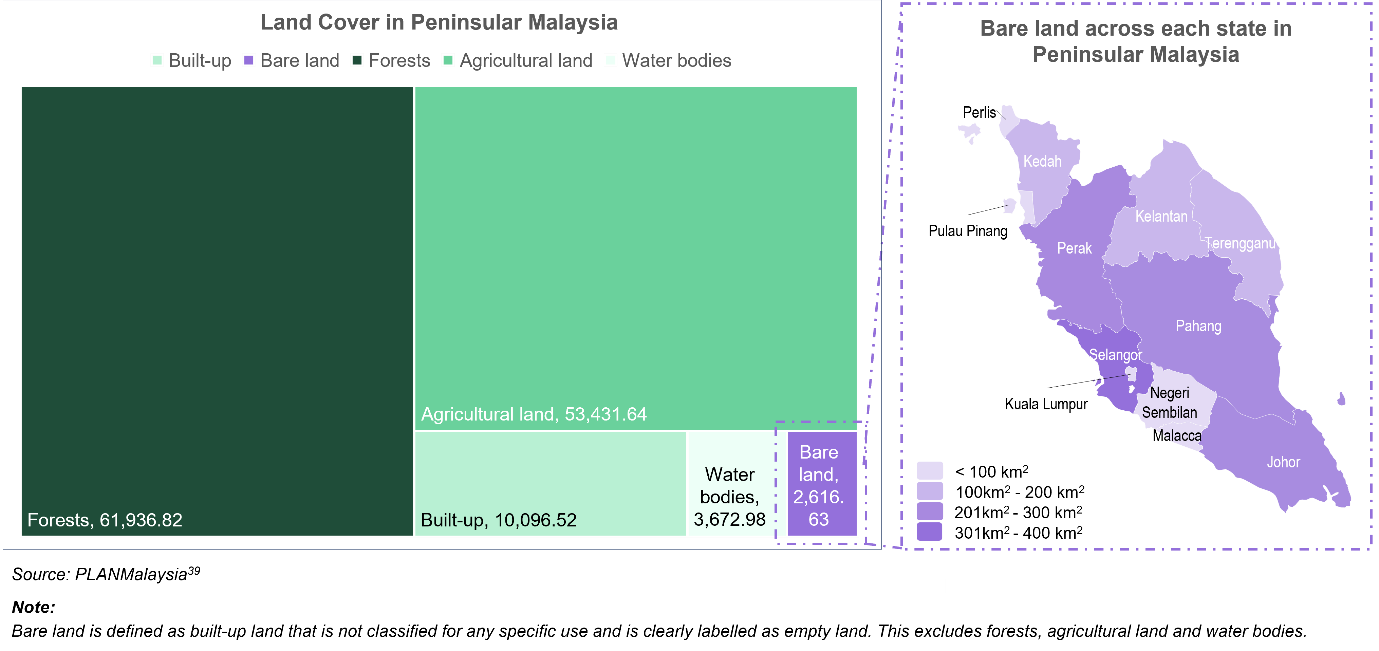

Peninsular Malaysia spans a total land area of 131,754.41 km2. This can be broadly categorised into four major land cover types: (1) built-up land, (2) forests, (3) agricultural land and (4) water bodies. According to the latest National Land Use Information Report 2022 published by PLANMalaysia,35 forests dominate at 47.01% of total land cover, followed by agricultural land at 40.55%, built-up land at 7.66% and water bodies at 2.79%. Among the built-up land, approximately 2,616.63 km2 has been identified as bare land, which is not classified for any specific use and is available for development. Fig. 2 shows the land cover types in Peninsular Malaysia and the breakdown of bare land available in each state in Peninsular Malaysia.

While large-scale deployment of renewable energy, especially solar power, requires a substantial amount of land, unregulated expansion may exceed the total empty land available in the region, potentially leading to conflicts with other land uses.36 In Malaysia, land use planning falls under state jurisdiction, with each state government determining permissible land uses based on its respective local planning and land use classifications. To allow a consistent land acquisition process for solar development, PLANMalaysia and the Ministry of Housing and Local Government have introduced the Garis Panduan Perancangan Pembangunan Ladang Solar (Planning Guidelines for Solar Farm Development), which outlines preferred land categories for solar deployment.37 Under the guidelines, industrial and agricultural lands are generally prioritised for ground-mounted solar projects, while water bodies are prioritised for floating solar applications. Development in environmentally sensitive areas and other restricted land categories is generally discouraged unless specifically permitted under state-level policies. While the guidelines provide an important reference to guide solar siting, land allocation and land use planning remain largely dependent on state-level decision-making based on local planning considerations and economic development objectives.38

Fig. 2. Land cover types and available bare land in Peninsular Malaysia

Note: Bare land is defined as built-up land that is not classified for any specific use and is labelled as empty land. This excludes forests, agricultural land and water bodies.

[ 4. Projected solar expansion and land use in Peninsular Malaysia ]

To understand how much new electricity capacity may be needed in the coming decades and what this could mean for land use in Peninsular Malaysia, this study applied the Regional Sustainable Energy Transition Planning (ReSET) model40 developed by a research team at Swinburne University of Technology Sarawak. The model was applied to examine the evolution of Peninsular Malaysia’s power system between 2025 and 2050 under two distinct future demand scenarios:

-

- NETR-aligned demand scenario, which reflects electricity demand growth prior to large-scale data centre expansion

- Data centre expansion (DCE) scenario, which incorporates additional demand associated with rapid data centre development

Several assumptions and planning constraints were incorporated into the model to ensure that the projected power system expansion remained realistic and reflected actual development conditions in Peninsular Malaysia. These include:

- Land use intensity: A solar power plant has a land use intensity of 0.0194 km² per MW of installed capacity.

- Empty bare land availability: The total area available for power generator deployment in each state was estimated as a weighted average of the proportion of state-level empty bare land and the estimated total unused suitable land (1,843 km2) for renewable energy deployment identified in MyRER.41

- States suitable for large-scale solar development: States with areas less than 20 km² of empty bare land were not considered for new ground-mounted solar development, which, in this case, are Perlis (6.19 km2) and Kuala Lumpur (17.58 km2).

- Natural gas constraint: Natural gas plant expansion was considered for areas adjacent to existing gas pipeline infrastructure42 and coastal water sources required for plant cooling.

- Hydropower constraint: Hydropower expansion was considered for states where hydropower facilities already exist and are planned, which are Kelantan, Pahang and Terengganu, due to the limited environmentally viable new hydro sites available in Peninsular Malaysia.43

- Technology deployment rate: Under the NETR target scenario, deployment rates were capped according to official national targets. Conversely, the DCE scenario allows for greater solar deployment to meet intensifying demand, starting at 2 GW annually in the initial period and increasing by an additional 2 GW every five years between 2031 and 2050.

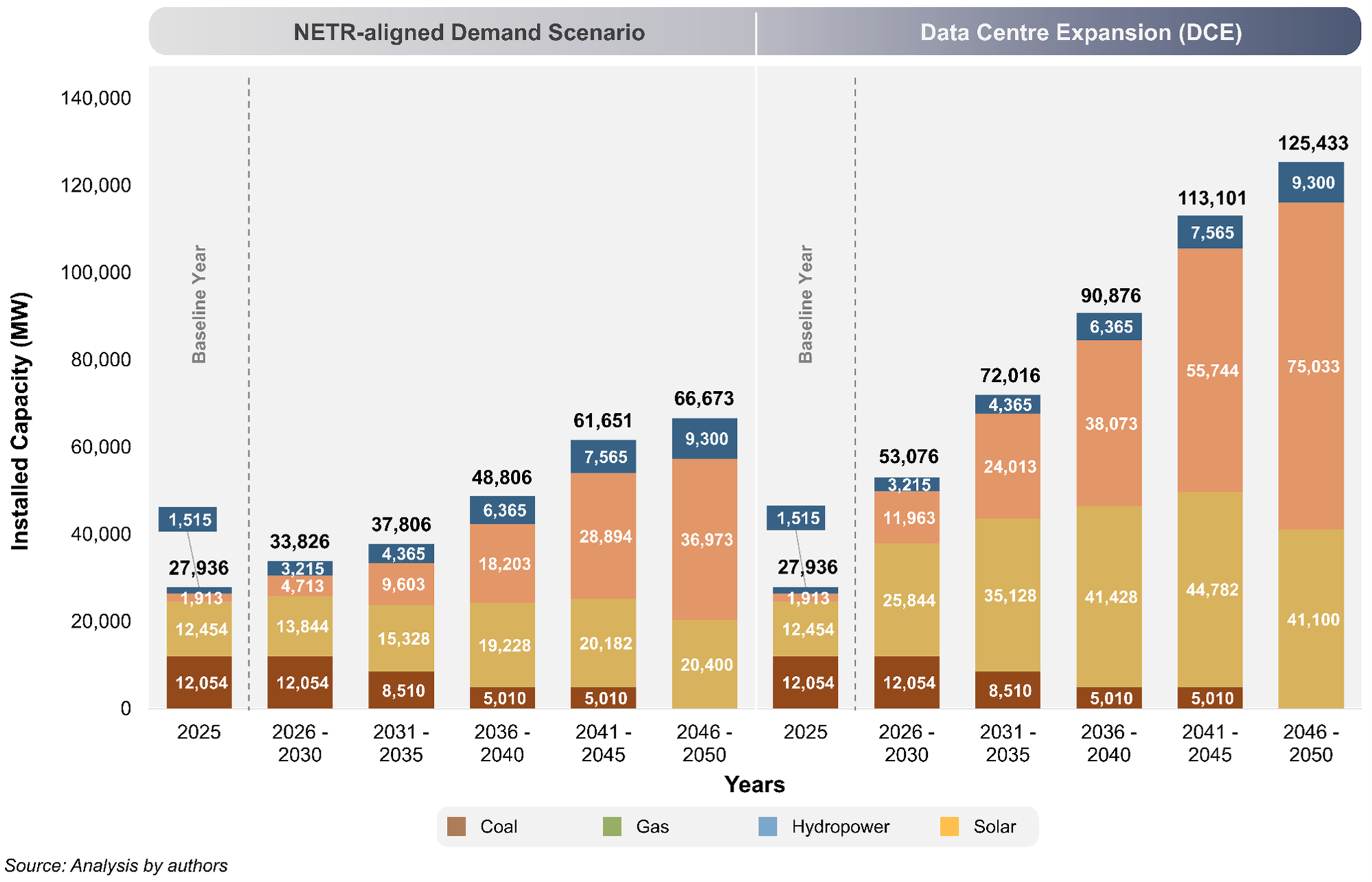

The ReSET model utilised the energy landscape in 2025 as the starting point to project future capacity expansion pathways that fulfil the electricity demand through 2050 in both scenarios. As of 2025, renewable energy contributions in Peninsular Malaysia remain relatively modest, with solar power and hydropower contributing to approximately 6.8% and 5.4% of the total installed generation capacity, respectively. Despite ongoing national energy transition ambitions, the power sector continues to be heavily dependent on fossil fuels, with coal and natural gas comprising 43.1% and 44.6% of the total installed capacity, respectively.

Moving across 2026 to 2050, as illustrated in Fig. 3, the total installed capacity under the NETR-aligned demand scenario is projected to more than double by 2050, increasing from approximately 27,936 MW in 2025 to 66,673 MW in 2046–2050. Such expansion is primarily driven by solar PV installation, with installed solar capacity projected to increase substantially from approximately 1,913 MW in 2025 to nearly 36,973 MW in 2046–2050. Throughout this transition, natural gas and hydropower are expected to continue playing a supporting role in the future electricity mix, accounting for 30.6% and 13.9% of installed capacity, respectively.

Fig. 3. Changes in installed capacity mix for NETR-aligned demand scenario (left panel) and DCE scenario (right panel)

Data centre growth could reshape Peninsular Malaysia’s future electricity capacity needs

When additional electricity demand from data centre expansion is considered under the DCE scenario, the total installed capacity is estimated to increase nearly twice the level projected under the NETR-aligned demand scenario. In this expanded installed capacity mix, solar PVs continue to dominate, accounting for close to 60% of total installed capacity, complemented by natural gas (32.8%) and hydropower (7.4%) in 2046–2050.

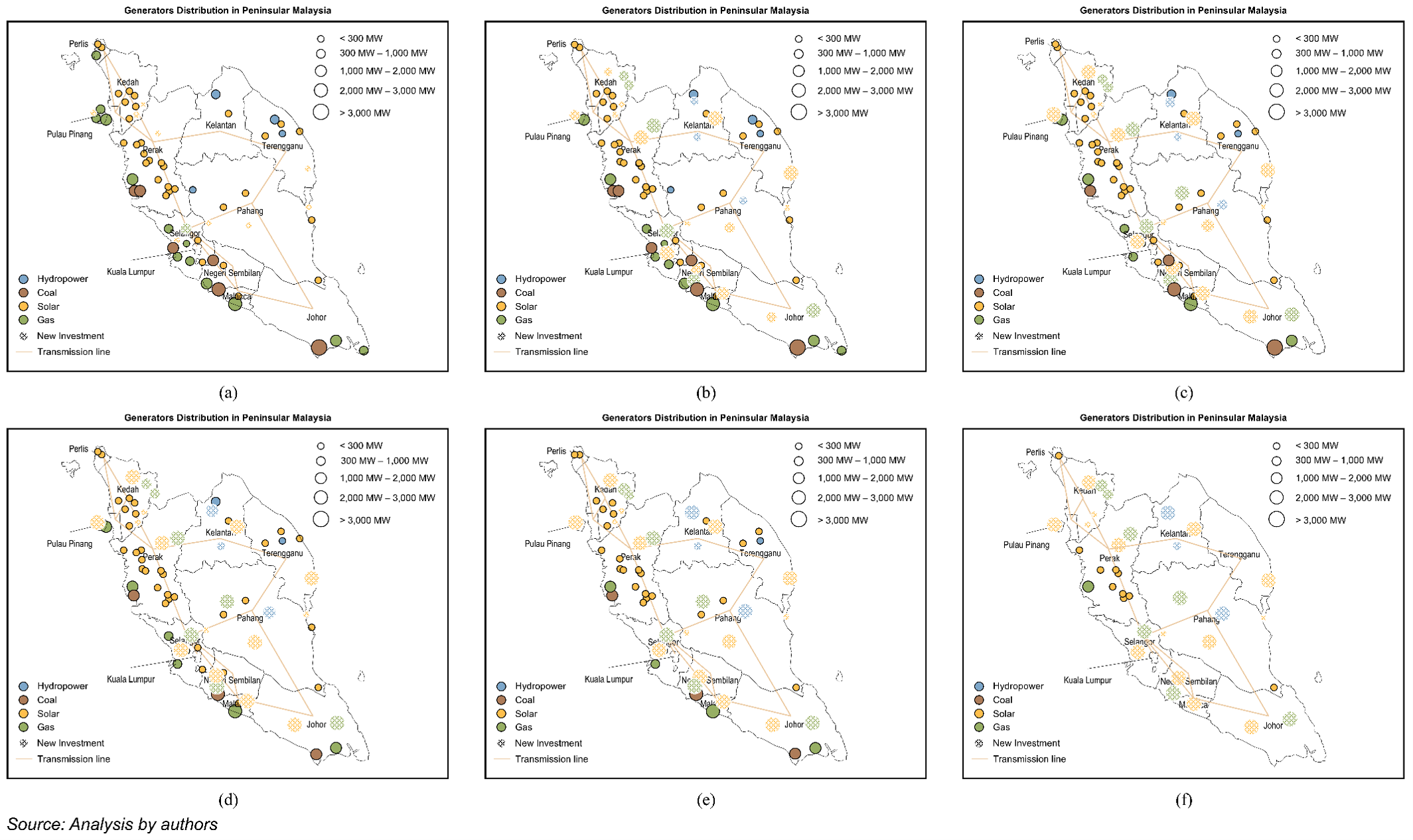

To achieve the required installed capacity, Fig. 4 shows that this expansion can be supported through the large-scale deployment of solar power generators across almost every state in Peninsular Malaysia, with the exceptions of Perlis and Greater Kuala Lumpur, where land availability remains limited. Other generation sources, such as natural gas, remain concentrated along the western coastal corridor, where existing gas infrastructure, industrial demand centres and access to cooling water provide operational advantages. On the other hand, hydropower facilities remain concentrated in the northeastern and central regions, as illustrated in Fig. 4.

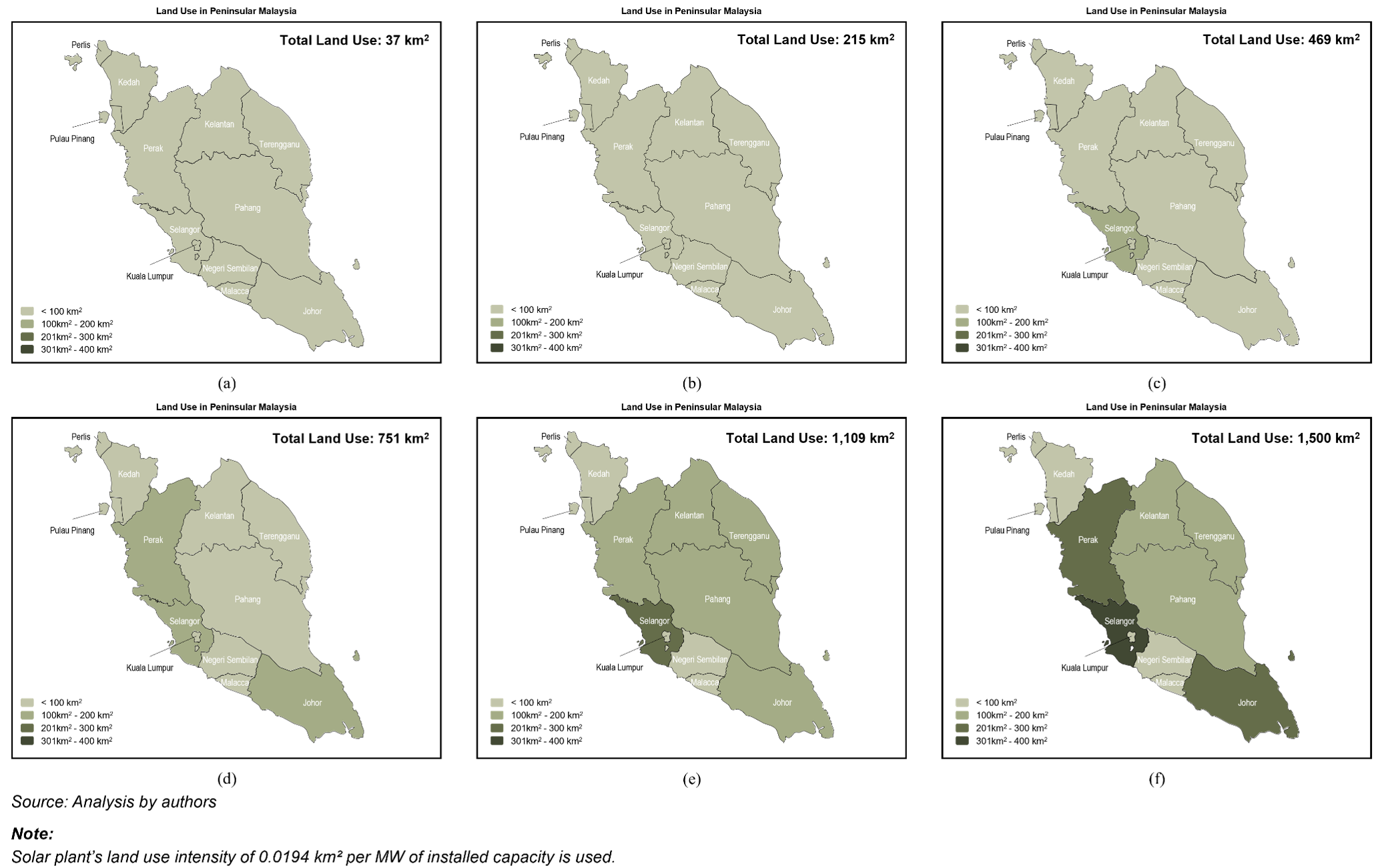

Translating the distribution of installed capacity into projected land requirements highlights the significant land use implications of meeting the rising electricity demand under the DCE scenario. Fig. 5 illustrates that the significant increase in installed capacity needs under the DCE scenario requires approximately 1,500 km² of cumulative land use between 2025 and 2050. Compared with the 730.2 km² of land use requirement under the NETR-aligned demand scenario, the analysis shows that an additional 769.8 km² of land, double the land use under the NETR-aligned demand scenario, is needed solely to support electricity demand attributed to rapid data centre growth. Fig. 5 illustrates the progressive breakdown of land use across each state in Peninsular Malaysia from 2025 to 2050 under the DCE scenario, highlighting the regional pressures in Peninsular Malaysia.

Overall, while the analysis highlights a substantial increase in both installed capacity and associated land requirements under the DCE scenario, the extent to which this land demand can be realised in practice is further shaped by implementation and planning constraints. Hence, it is important to further examine the real-life land use planning challenges that may influence the actual deployment of large-scale solar capacity in Peninsular Malaysia, as discussed in the next section.

Fig. 4. Distribution of generators in Peninsular Malaysia: (a) 2025, (b) 2026–2030, (c) 2031–2035, (d) 2036–2040, (e) 2041–2045 and (f) 2045–2050

Fig. 5. Total land use in each state: (a) 2025, (b) 2026–2030, (c) 2031–2035, (d) 2036–2040, (e) 2041–2045 and (f) 2045–2050

[ 5. Land use challenges for large-scale solar deployment ]

As electricity demand continues to rise, particularly under rapid data centre expansion, the amount of land that is realistically suitable, accessible and available for large-scale solar development is becoming increasingly constrained. These limitations arise not only from physical land scarcity but also from competing development priorities, climate and ecological risks, governance and approval processes, and emerging infrastructure requirements associated with the next phase of the energy transition. In this section, key land-use and implementation challenges that may affect the scalability of large-scale solar deployment in Peninsular Malaysia are discussed.

5.1 Challenges of land suitability criteria

Although Peninsular Malaysia has 1,843 km2 of unused suitable land available for large-scale solar deployment, the actual amount of suitable land is substantially smaller once planning, environmental, technical and infrastructure constraints are considered. In practice, not all empty land can be readily converted into solar sites. The Planning Guidelines for Solar Farm Development issued by PLANMalaysia and the Ministry of Housing and Local Government provide a structured framework for solar siting and land suitability assessment.44 Under these guidelines, ground-mounted solar farms are generally permitted on industrial land, brownfield areas, ex-mining land and selected agricultural land, particularly lower productivity agricultural areas classified as Class 3, 4 or 5. On the other hand, development on productive agricultural land, such as paddy cultivation areas, environmentally sensitive areas, urban centres, permanent food production parks, and land with ecological or historical significance, is restricted.

Beyond broader planning considerations, several technical factors further constrain the suitability of land for large-scale solar deployment. Utility-scale solar projects typically require a relatively flat terrain, large contiguous land parcels and proximity to substations or transmission infrastructure to remain economically viable.45 Sites that are fragmented, unevenly distributed or located far from existing grid infrastructure are generally less attractive, as substantial additional infrastructure investment may be required, which increases overall project costs. In many states, particularly those with strong industrial and economic growth, many of the strategically located sites that satisfy both zoning and infrastructure requirements have already been utilised during previous LSS bidding cycles.46 The remaining sites are often smaller, fragmented or located in less favourable areas, reducing their attractiveness for future development.

Climate vulnerability affecting long-term site suitability of solar development

Climate-related risks are becoming increasingly important considerations in determining the long-term suitability of land for solar deployment in Malaysia. According to the International Disaster Database, floods represent Malaysia’s most frequent natural disaster, accounting for approximately 85% of all recorded natural disasters since 2000.47 Malaysia has experienced, on average, one to two large-scale flood events annually over the same period, with major flooding events occurring more frequently approximately every seven years.48 Certain regions in Peninsular Malaysia, particularly Greater Kuala Lumpur and Penang, are increasingly exposed to flood hazards due to rapid urban expansion that leads to deforestation and insufficient drainage.49 Locating ground-mounted solar facilities in flood-prone areas may expose projects to operational disruptions, infrastructure damage, accelerated equipment degradation and higher long-term maintenance costs.

Consequently, land that appears technically suitable from a spatial planning and infrastructure perspective could become increasingly vulnerable when long-term climate exposure is factored into the planning process. Incorporating climate-risk screening and resilience assessment into future solar planning processes may therefore further reduce the amount of land considered suitable for large-scale solar deployment across the region.

Ecological constraints and human-wildlife conflicts in solar siting

Ecological considerations further narrow the amount of land that can be realistically utilised for large-scale solar deployment. Solar projects located near forest reserves, ecological corridors, wetlands and wildlife habitats may contribute to habitat fragmentation, disrupt ecological connectivity and increase the risk of human-wildlife interactions. For instance, the Bukit Selambau Solar Park in Kedah has encountered challenges associated with its proximity to habitats inhabited by long-tailed macaques.50 As surrounding land use changes continue to alter natural habitats, these adaptable primates have increasingly ventured into nearby human activity areas in search of food, contributing to rising human-wildlife conflicts. Similar concerns may emerge in other regions wherever future solar development overlaps with ecologically sensitive landscapes or wildlife movement corridors. As a result, when ecological safeguards, such as human-wildlife conflict considerations, are incorporated into future solar siting assessments, the pool of deployable land is further reduced.

In summary, the interplay of planning, technical, climate and ecological constraints indicates that the amount of land that is realistically deployable for large-scale solar development is substantially smaller than the amount of undeveloped land that may appear available from a purely spatial perspective. As future electricity demand continues to rise, land suitability limitations are expected to emerge as one of the most significant structural constraints affecting the scalability of solar deployment in Peninsular Malaysia.

5.2 Challenges of land competition

While solar energy forms a central pillar of Malaysia’s long-term decarbonisation strategy, the land required to support this transition increasingly overlaps with areas targeted for other forms of economic development. This challenge is particularly evident in rapidly developing states, such as Johor and Selangor, where rising electricity demand is occurring alongside accelerated industrialisation, logistics development, urban expansion and large-scale data centre investments. These sectors frequently compete for the same strategically located land areas that are most suitable for solar deployment, particularly sites with good transportation access, grid connectivity and a relatively flat terrain.

This growing scarcity of strategically located land has encouraged several states to explore alternative land-use approaches for solar energy deployment, including the use of plantation land and brownfield sites. For instance, the Kedah state government has announced plans to utilise selected oil palm plantation areas for solar energy development as part of its broader renewable energy ambitions.51 Such developments illustrate how increasing land competition is beginning to reshape renewable energy planning and land allocation decisions in Peninsular Malaysia.

This indicates that future solar expansion will increasingly need to compete with other strategic land uses. As a result, without more integrated land use planning and alternative deployment strategies, land competition may become one of the key limiting factors affecting the pace and scalability of Malaysia’s renewable energy transition.

5.3 Challenges of land governance and administrative processes

Even when technically suitable land is available, the process of securing and mobilising land for solar development remains administratively complex and varies significantly across states. In practice, solar developers often rely on land agents, private networks or independent searches to identify potential sites suitable for solar project developments. Information relating to land ownership, zoning classifications and future development plans is not always readily accessible. Although national guidelines for solar siting have been introduced, land administration and development approvals remain under state jurisdiction.52 This results in considerable variation in regulations, approval procedures, land title conversion requirements, and administrative practices across different states in Peninsular Malaysia. Consequently, sites that initially appear technically feasible may later encounter ownership disputes, zoning incompatibilities or unforeseen planning restrictions. As a result, the amount of land that can be realistically mobilised for solar deployment is often a mere fraction of what appears technically suitable from a purely spatial perspective.

The varying land governance across each state also reflects a broader disconnect between national renewable energy ambitions and state-level development priorities. While national policies, such as the NETR, position solar energy as a key pillar of Malaysia’s long-term energy transition, decisions relating to land allocation and zoning remain largely influenced by state-level economic and development priorities. In some cases, land suitable for solar deployment may already be earmarked for industrial expansion, urban development, tourism or agricultural activities under existing state and local development plans. Such challenges are expected to become increasingly significant as Peninsular Malaysia accelerates both economic development and decarbonisation efforts simultaneously.

These governance and administrative bottlenecks suggest that future solar energy expansion will require stronger coordination between federal and state governments, greater transparency in land-related processes and more integrated spatial-energy planning frameworks. Without such improvements, institutional and administrative barriers may continue to constrain the efficiency and scalability of large-scale solar deployment in Peninsular Malaysia.

5.4 Challenges of integrated solar-battery deployment

As energy from solar PVs remains inherently intermittent, increasing attention is placed on battery energy storage systems (BESSs) as a key enabling technology for higher renewable energy penetration. Energy storage enhances grid flexibility, manages solar variability, supports peak demand balancing and improves system reliability. In Malaysia, this direction is gaining momentum through a series of emerging national and regional initiatives.

Through the Energy Commission, the government has introduced the Malaysia Battery Energy Storage System programme, a national BESS procurement initiative targeting the commercial operation of four projects by 2026.53 In parallel, the World Bank Group has committed support to the Southern Johor Renewable Energy Corridor, with a plan to integrate approximately 4 GW of solar PVs and 5.12 GWh of battery storage near Malaysia’s southern border with Singapore.54 At the utility and distribution levels, several pilot and demonstration projects are already underway. Tenaga Nasional Berhad has initiated Malaysia’s first 400MWh utility-scale BESS project, operated by Grid System Operator and overseen by the Energy Commission.55 In parallel, a Community Energy Storage System has been deployed in collaboration with Sime Darby Property Berhad at the City of Elmina’s Ilham Residence, totalling approximately 0.4 MW of capacity across pilot sites.56 These developments reflect the growing recognition of BESSs as a central component in enabling large-scale renewable energy deployment in Malaysia.

Depending on system design and configuration, utility-scale BESS facilities are estimated to require approximately 0.00012–0.0004 km2/MW installed capacity.57 While the physical footprint of the battery units themselves is relatively small, the necessity for strategic positioning near substations and transmission hubs means that the integration of solar PVs with BESSs may further intensify competition for strategically located land, further complicating the spatial planning for further complicating the spatial planning for large-scale solar deployment.

[ 6. Summary of key findings and recommendations ]

To address the land use challenges associated with large-scale solar deployment identified in the previous section, a set of recommendations to reduce land use challenges in Peninsular Malaysia is proposed in this section. These recommendations focus on expanding alternative deployment pathways to improve land use efficiency, while balancing energy transition objectives with competing spatial, environmental and development constraints.

Recommendation 1: Repower retired solar PV sites

An alternative strategy for land preservation is the “repowering” of existing solar sites. Repowering is the process of upgrading or replacing ageing solar generators to extend the operational life of an established facility. It has increasingly gained attention in various countries, such as Italy58 and the United States.59 Rather than developing new greenfield projects, repowering involves replacing or upgrading existing solar power generators to extend their lifetime on the same site.60 This approach enables developers to extend project lifetimes, enhance performance and utilise existing infrastructure, which reduces development costs61 and increases land use efficiency.62 In this study, solar repowering was analysed by assuming that land occupied by existing solar plants reaching the end of their operational lifespan is immediately available for the redevelopment of new solar projects, allowing new solar capacity on the same site.

The analysis shows that deploying new solar plants on retired solar sites reduces total land use by 21.95 km² relative to the DCE demand scenario without repowering. This reduces land use intensity from 0.01998 km²/MW to 0.01969 km²/MW, demonstrating a reduction in land use intensity of 0.0003 km²/MW (equivalent to 1.4% reduction). While this reduction may appear modest in the near term, the benefits would compound significantly over a longer planning horizon. Preliminary estimates suggest that if all existing solar sites were repowered with new capacity additions, up to 37.06 km² of land could potentially be reused, which may reduce the need for new land and lower the land use intensity to 0.01887 km²/MW for the same amount of installed capacity. Nevertheless, it is worth noting that this analysis conservatively assumes that the new solar panels installed at repowered plants are associated with the same efficiency compared with that of the retired solar panels. When modern PV modules with higher efficiency (i.e., greater output per unit area) are deployed, this could further reduce the land use intensity.63

Recommendation 2: Enhance land use efficiency through technological innovation

At present, most existing photovoltaic systems operate below their theoretical efficiency ceiling, known as the Shockley-Queisser limit, which restricts the potential output of solar technology, such as single-junction crystalline silicon solar cells, to approximately 33%.64 As installation density grows, improving conversion efficiency becomes a central strategy for reducing land use. Recent laboratory advancements have demonstrated that theoretical efficiency potentials between 50% and 60% are achievable by inhibiting light conversion to heat at low temperatures.65 These findings indicate that future generations of solar modules could deliver nearly twice the energy output within the same spatial footprint, substantially easing land pressure associated with the expansion of large-scale solar projects.

This trend underscores the need to strengthen domestic research and innovation to support the transition towards higher-efficiency photovoltaic technologies. In Peninsular Malaysia, the Solar Energy Research Institute at National University Malaysia has already established a foundation in advanced energy conversion systems, advanced solar thermal technology and advanced solar cells. With targeted funding and strategic coordination, the institute and other national laboratories could expand their research into emerging cell architectures and/or system designs that can enhance solar energy conversion efficiency.

On top of that, partnerships between research institutions, the private sector and international technology developers could also accelerate the localisation and commercial application of advanced photovoltaic innovations. International experience provides useful reference points. In the United States, the Department of Energy’s Solar Energy Technologies Office funds research and development in high-efficiency photovoltaics, agrivoltaics and solar-plus-storage integration.66 These initiatives demonstrate how consistent public funding, coupled with structured technology transfer, can rapidly scale emerging innovations from laboratory research to industry deployment.

From a policy standpoint, Malaysia’s future large‑scale solar procurement rounds should consider integrating technology‑based performance criteria that reward projects achieving higher energy yield per hectare. Incorporating such parameters into the LSS evaluation framework would mark a transition from capacity‑driven expansion to productivity‑based deployment. Doing so would not only optimise land utilisation but also position Malaysia’s solar sector to adopt advanced technologies that strengthen long‑term competitiveness and sustainability.

Recommendation 3: Scale up floating solar development

Malaysia has already begun charting a clear pathway towards floating solar PV deployment as part of its broader renewable energy expansion strategy. In the latest LSS5+ bidding cycle, a dedicated 500 MW quota was allocated for floating solar projects, signalling strong policy recognition of floating solar technology’s role in diversifying deployment options.67 Within this allocation, 200 MW has been tendered for development at the Chereh Dam in Kuantan.68 In parallel, Cypark Resources Berhad is expected to develop a large-scale floating solar project at Tasik Kenyir in partnership with Tenaga Nasional Berhad (TNB), forming part of TNB’s broader 2.5GW Hybrid Hydro-Floating Solar initiative.69

From a regulatory perspective, floating solar deployment is also formally supported under Malaysia’s planning framework. The Planning Guidelines for Solar Farm Development issued by PLANMalaysia and the Ministry of Housing and Local Government provide guidelines for floating solar siting.70 This includes suitable water bodies, such as abandoned mining lakes, ex-mining ponds and hydro reservoirs. These developments are, however, subject to environmental safeguards, with exclusions for environmentally sensitive areas, such as coastal zones, water catchments and drinking water reserves. Collectively, these regulatory references constitute a foundation for the expansion of floating solar PVs across Peninsular Malaysia.

The attractiveness of floating solar deployment lies primarily in its ability to expand renewable energy capacity without competing for scarce terrestrial land resources. By utilising existing water bodies, floating solar deployment reduces pressure on land availability, while also offering potential co-benefits, such as reduced water evaporation and improved panel efficiency due to cooling effects.71 Globally, early adopters, such as Japan and Indonesia, have demonstrated the technical and economic viability of this technology. As highlighted by the World Economic Forum, Japan has become one of the leading countries in floating solar deployment, driven by limited land availability and the presence of numerous reservoirs and artificial water bodies suitable for development.72

In Malaysia’s context, these developments suggest that floating solar PVs can play a strategically important role in alleviating land constraints associated with large-scale solar deployment. Given the growing competition for suitable land illustrated under the DCE scenario, floating solar deployment offers a complementary pathway that can reduce pressure on terrestrial sites, while still supporting national renewable energy targets. To further accelerate deployment, Malaysia could strengthen this trajectory by expanding dedicated floating solar quotas in future LSS bidding cycles. On top of that, the identification and mapping of suitable water bodies should be prioritised to expedite the land acquisition process for floating solar adoption.

Recommendation 4: Promote dual-land use and agrivoltaic systems

A more integrated approach to land utilisation can be achieved through dual-use development models, commonly referred to as agrivoltaics. This concept enables the simultaneous use of the same land area for both solar energy generation and agricultural production. By providing partial shading, solar panels can help reduce heat stress on crops and livestock, improve microclimatic conditions and enhance resilience against drought conditions.73 In addition, agrivoltaic systems can improve land use efficiency by maintaining agricultural output, while generating renewable electricity, with additional co-benefits reported in terms of reduced water demand and improved farm productivity through better land management practices.74,75

The concept has been operationalised in Japan through a practice known as “solar sharing”, which integrates solar panels with active agricultural land use.76 Developed by the Japanese entrepreneur and agricultural machinery engineer Akira Nagashima and first introduced in 2004 in Chiba Prefecture, Japan, the approach is designed to address land scarcity by enabling simultaneous food and energy production on the same plots of land. This is particularly relevant in Japan, where approximately two-thirds of the land area is mountainous and the availability of flat, arable land is limited, creating strong competition between agricultural, urban and energy uses. Estimates suggest that if solar sharing were expanded to cover an additional 10% of Japan’s approximately 4.77 million hectares of agricultural land, it could potentially supply up to 37% of the country’s electricity demand.77 This highlights the significant system-level contribution that dual-use land strategies can offer when scaled effectively.

In Malaysia’s context, agrivoltaics presents a complementary pathway to conventional ground-mounted solar deployment, particularly in areas where agricultural land overlaps with high-solar-potential regions. By enabling co-location of food and energy production, this approach could help alleviate land competition pressures, while enhancing rural productivity and climate resilience. To further support its adoption, Malaysia may consider developing targeted regulatory frameworks, pilot-scaling demonstration projects and introducing incentive mechanisms that encourage integration between agricultural stakeholders and renewable energy developers. Financial incentives, including tax credits, land lease discounts or soft loans under the Green Technology Financing Scheme, can be targeted to encourage adoption by landowners and plantation operators. Pilot projects co-developed with the Department of Agriculture or the Malaysian Palm Oil Board would be essential to provide the performance data needed to establish a blueprint for a land-efficient, decentralised energy future.

[ Abbreviations ]

BESS |

Battery energy storage system |

CGPP |

Corporate Green Power Programme |

CRESS |

Corporate Renewable Energy Supply Scheme |

DCE |

Data centre expansion |

PLANMalaysia |

Department of Town and Country Planning |

GW |

Gigawatt |

LSS |

Large-Scale Solar |

MyRER |

Malaysia Renewable Energy Roadmap |

MW |

Megawatt |

NETR |

National Energy Transition Roadmap |

NEM |

Net Energy Metering |

ReSET |

Regional Sustainable Energy Transition Planning |

SARE |

Supply agreement for renewable energy |

TNB |

Tenaga Nasional Berhad |

VPPA |

Virtual power purchase agreement |

[ Contributors ]

Cheng Xin Hui is a researcher pursuing her PhD at SUTS. She specialises in macro-scale energy planning and decarbonisation pathway development for national-level and state-level planning. Her research focuses on leveraging mathematical models to translate technical insights into actionable policy recommendations, with particular emphasis on low-carbon energy integration, negative emissions technologies and resource utilisation trade-offs in energy transition planning.

Dr How Bing Shen is an Associate Professor and the Associate Dean of Research and Development at Swinburne University of Technology Sarawak (SUTS). He is a leading researcher in sustainable process integration, circular economy and macro-scale planning, with work that has informed decarbonisation strategies for the energy, palm oil and waste sectors. He serves as the Vice-President of the International Institute for P-graph and holds editorial appointments with several international peer-reviewed journals. His contributions to the field have earned him multiple accolades, including the 2021 IChemE Global Young Researcher Award and recognition as one of the world’s Top 2% Scientists in 2025.

Dr Viknesh Andiappan is a Professor and Associate Director of the School of Research at SUTS. He is a specialist in industrial decarbonisation and energy systems optimisation, with a research focus on developing computational tools and algorithms to design net-zero energy systems and supply chains. He leads the Sustainable and Clean Energy Research Cluster at SUTS and previously served as the Chair of IChemE’s Palm Oil Processing Special Interest Group. His work in the field was notably recognised with the 2023 National Outstanding Young Researcher Award.

[ Illustrator ]

Keely Chan is an illustrator based in Kuala Lumpur who is known for creating the IP Book of Kelu, an original IP centred around travel content and visual storytelling. Through her illustrations, she captures experiences, cultures, and destinations in a playful and imaginative way, combining art and travel to create engaging narratives that resonate with audiences who enjoy exploration and creativity.

[ REFERENCES ]

1Economic Planning Unit. (n.d.). Twelfth Malaysia Plan. https://rmke12.ekonomi.gov.my/en

2Sustainable Energy Development Authority Malaysia. (n.d.). Malaysia Renewable Energy Roadmap (MyRER). https://www.seda.gov.my/reportal/myrer/

3Economic Planning Unit. (n.d.). National Energy Policy, 2022–2040. https://ekonomi.gov.my/sites/default/files/2022-09/National_Energy_Policy_2022-2040.pdf

4Ministry of Economy. (n.d.). National Energy Transition Roadmap. https://ekonomi.gov.my/sites/default/files/2023-09/National%20Energy%20Transition%20Roadmap_0.pdf

6 Sustainable Energy Development Authority Malaysia. (n.d.). Malaysia Renewable Energy Roadmap (MyRER). https://www.seda.gov.my/reportal/myrer/

7Wood Mackenzie (2025). Feeding the Cloud: Data Centre Power Demand in Southeast Asia. https://go.woodmac.com/l/131501/2025-12-09/355hc8/131501/1765257884wj6SVzDi/Wood_Mackenzie_Extract_Feeding_the_cloud_data_center_power_demand_in_S.pdf

8Bank Negara Malaysia. (2025). BNM Quarterly Bulletin, 41, 3. https://www.bnm.gov.my/documents/20124/19910400/qb25q3_en_book.pdf

9Zhang, P., et al. (2024). Revisiting the land use conflicts between forests and solar farms through energy efficiency. Journal of Cleaner Production, 434, 139958. https://doi.org/10.1016/j.jclepro.2023.139958

10Sustainable Energy Development Authority Malaysia. (n.d.). Renewable Energy Act 2011. https://www.seda.gov.my/policies/renewable-energy-act-2011/

11Energy Commission. (n.d.). Large-Scale Solar Photovoltaic. https://www.st.gov.my/procurement/large-scale-solar-photovoltaic

12Sustainable Energy Development Authority Malaysia. (n.d.). Net Energy Metering (NEM) 3.0. https://www.seda.gov.my/reportal/nem/

13Tenaga Nasional Berhad. (n.d.). Self-Consumption (SELCO). https://www.mytnb.com.my/renewable-energy/self-consumption

14Energy Commission. (n.d.) Large-Scale Solar Photovoltaic. https://www.st.gov.my/procurement/large-scale-solar-photovoltaic

15XPlus Energy (n.d.). Large-Scale Solar (LSS) Malaysia: Development, EPC & Investments. https://www.plusxnergy.com/large-scale-solar/

16Jowett, P. (2025, October 9). Over 6 GW of solar approved under Malaysia’s large-scale solar program. PV Magazine. https://www.pv-magazine.com/2025/10/09/over-6-gw-of-solar-approved-under-malaysias-large-scale-solar-program/

17Sustainable Energy Development Authority Malaysia. (n.d.). Net Energy Metering (NEM) 3.0. https://www.seda.gov.my/reportal/nem/

18Sustainable Energy Development Authority Malaysia. (n.d.). NEM 3.0 FAQs. https://www.seda.gov.my/reportal/nem/nem3-faq/

19Sustainable Energy Development Authority Malaysia. (n.d.). Malaysia Renewable Energy Roadmap (MyRER). https://www.seda.gov.my/reportal/myrer/

21Single Buyer. (n.d.). Corporate Green Power Programme. https://www.singlebuyer.com.my/market/market-operations/programs/cgpp

22Energy Commission. (n.d.) Corporate Renewable Energy Supply Scheme (CRESS). https://www.st.gov.my/sustainability/energy-transition-programmes/corporate-renewable-energy-supply-scheme-cress

23Tenaga Nasional Berhad. (n.d.). Solar for Rakyat Incentive Scheme (SolaRIS). https://www.tnb.com.my/solar-for-rakyat-incentive-scheme-solaris/

24Energy Commission. (n.d.). Guidelines for Community Renewable Energy Aggregation Mechanism (CREAM). https://www.st.gov.my/contents/2025/CREAM/CREAM%20GUIDELINE_FINAL.pdf

25Sustainable Energy Development Authority Malaysia. (n.d.). NEM 3.0 FAQs. https://www.seda.gov.my/reportal/nem/nem3-faq/

26Sustainable Energy Development Authority Malaysia. (n.d.) Solar Accelerated Transition Action Programme (Solar ATAP). https://www.mytnb.com.my/renewable-energy/solar-accelerated-transition-action-programme

27Peninsular Malaysia’s rising demand for more power generation capacity. (2025, October 17). The Star. https://www.thestar.com.my/business/business-news/2025/10/17/rising-demand-for-more-power-generation-capacity

30Malaysian Investment Development Authority. (2025). Guideline for Sustainable Development of Data Centre. https://www.mida.gov.my/wp-content/uploads/2024/12/Guideline-for-Sustainable-Development-of-Data-Centre.pdf

31Single Buyer. (n.d.). Current Demand. https://www.singlebuyer.com.my/

32Energy Commission. (2020). National Energy Balance 2020. https://www.st.gov.my/resources/national-energy-balance-2020

33Ministry of Energy Transition and Water Transformation Malaysia. (2025). Power Development Plan (PDP) in Peninsular Malaysia. https://www.egnret.ewg.apec.org/Upload/202505231324450ae4831.pdf

34Palansamy, Y. (2025, February 27). Putrajaya: Data centres could need more power by 2040 than Malaysia uses annually now. Malay Mail. https://www.malaymail.com/news/malaysia/2025/02/27/putrajaya-data-centres-could-need-more-power-by-2040-than-malaysia-uses-annually-now/168145

35PLANMalaysia. (2022). Laporan Maklumat Guna Tanah Negara 2022 [National Land Use Information 2022]. https://myplan.planmalaysia.gov.my/portal-main/publication-details?id=19

36Zhang, P., et al. (2024). Revisiting the land use conflicts between forests and solar farms through energy efficiency. Journal of Cleaner Production, 434, 139958. https://doi.org/10.1016/j.jclepro.2023.139958

37PLANMalaysia and Ministry of Housing and Local Government. (2025). Garis Panduan Perancangan Pembangunan Ladang Solar [Planning Guidelines for Solar Farm Development]. https://www.planmalaysia.gov.my/uploads/content-downloads/file_20251114204500.pdf

38Sahid, M. S., Suratman, R., & Mohd Ali, H. (2021). Acquiring elements of solar farm development’s approval consideration in Johor. Planning Malaysia Journal, 19(4), 72–82. https://doi.org/10.21837/pm.v19i18.1034

40Cheng, X. H., et. al. (2026). Optimal energy transition planning: Navigating the trade-offs between short-term and long-term decision-making. Industrial & Engineering Chemistry Research. Advance online publication. https://doi.org/10.1021/acs.iecr.5c03999

41Sustainable Energy Development Authority Malaysia. (n.d.). Malaysia Renewable Energy Roadmap (MyRER). https://www.seda.gov.my/reportal/myrer/

42Malaysian Gas Association. (n.d.). Malaysian Gas Map. https://malaysiangas.com/2023/11/16/malaysian-gas-map/

43Grid System Operator. (n.d.). Power Station Information. https://www.gso.org.my/SystemData/PowerStation.aspx

46Energy Commission. (n.d.). Large-scale solar photovoltaic. https://www.st.gov.my/procurement/large-scale-solar-photovoltaic

47Centre for Research on the Epidemiology of Disasters. (n.d.). International Disaster Database. https://www.emdat.be/

48World Bank Group. (n.d.). Climate Change Knowledge Portal. https://climateknowledgeportal.worldbank.org/

49Bank Negara Malaysia. (2023). Financial Stability Review — Second Half 2023. https://www.bnm.gov.my/documents/20124/13790687/fsr23h2_en_book.pdf

50Tenaga Nasional Berhad. (2017). TNB’s Solar Park: Advancing Clean Energy with Environmental Responsibility. https://www.tnb.com.my/sustainability/esg-stories-tnb-solar-park

51Zulkifli, A. (2025, March 21). Kedah poised to be regional solar power hub. New Straits Times. https://www.nst.com.my/news/nation/2025/03/1191171/kedah-poised-be-regional-solar-power-hub

53Colthorpe, A. (2026, January 8). Malaysia: Energy Commission shortlists bidders in 1.6GWh “landmark” BESS programme. Energy Storage News. https://www.energy-storage.news/malaysia-energy-commission-shortlists-bidders-in-1-6gwh-landmark-bess-programme/

54Norman, W. (2025, December 2). World Bank supports multi-gigawatt cross-border renewable energy project in Malaysia. Energy Storage News. https://www.energy-storage.news/world-bank-supports-multi-gigawatt-cross-border-renewable-energy-project-in-malaysia/

55Tenaga Nasional Berhad. (n.d.). Empowering Sustainable Future: TNB’s Solar Panel & Battery Management Strategies. https://www.tnb.com.my/sustainability/tnb-solar-panel-battery-management-strategies

56Sime Darby Property, TNB launches Malaysia’s first community solar initiative under NETR. (2025, April 28). The Edge Malaysia. https://theedgemalaysia.com/node/753254

57Great Plains Institute. (n.d.). Fact Sheet: Battery Energy Storage Systems and Land Use. https://www.extension.iastate.edu/communities/files/documents/GPI%20BESS%20Fact%20Sheet%20on%20Land%20Use.pdf

58Trepin, E. (2026, January 27). How Italy is repowering aging solar into assets. RatedPower. https://ratedpower.com/blog/italy-repowering-solar/

59Morato, E. (2025, October 7). Repowering aging U.S. solar farms: A strategic pivot in a changing energy landscape. PV Magazine. https://pv-magazine-usa.com/2025/10/07/repowering-aging-u-s-solar-farms-a-strategic-pivot-in-a-changing-energy-landscape/

60Wyatt, J. (2020, April 1). Repowering and decommissioning: What happens in communities when solar and wind projects end? Great Plains Institute. https://betterenergy.org/blog/repowering-and-decommissioning-what-happens-in-communities-when-solar-and-wind-projects-end/

62Herceg, S., Fischer, M., Weiß, K.-A., & Schebek, L. (2022). Life cycle assessment of PV module repowering. Energy Strategy Reviews, 43, 100928. https://doi.org/10.1016/j.esr.2022.100928

63Yin, Y., et al. (2024). Improving land-use efficiency of solar power in China and policy implications. Solar Energy, 280, 112867. https://doi.org/10.1016/j.solener.2024.112867

64Zanatta, A. R. (2022). The Shockley–Queisser limit and the conversion efficiency of silicon-based solar cells. Results in Optics, 9, 100320. https://doi.org/10.1016/j.rio.2022.100320

66Department of Energy. (n.d.). Solar Energy Research Areas. https://www.energy.gov/cmei/systems/solar-energy-research-areas

67Energy Commission. (2025). Notis Makluman Pelaksanaan Program Bidaan Terbuka LSS Petra 5+ [Notice of Implementation of LSS Petra 5+ Open Bidding Programme]. https://www.st.gov.my/sites/default/files/2026-03/Notis-Makluman-Pelaksanaan-Bidaan-Terbuka-LSS-PETRA-5%2B_17-Januari-2025.pdf

68Tenaga Nasional Berhad. (2025). Floating Solar Project to Become Region’s Largest. https://www.tnb.com.my/assets/newsclip/25122025a.pdf

69Zainul, I. F. & Cheng, J. (2026, April 3). Cypark tipped to bag RM2b contract for Tasik Kenyir floating solar farm. The Edge Malaysia. https://theedgemalaysia.com/node/798489

71Goh, K. C., et al. (2026). Harnessing floating solar power to decarbonize Southeast Asia’s energy sector for carbon neutrality. Solar Energy, 303, 114079. https://doi.org/10.1016/j.solener.2025.114079

72Broom, D. (2019, March 2022). How Japan became the world leader in floating solar power. World Economic Forum. https://www.weforum.org/stories/2019/03/japan-is-the-world-leader-in-floating-solar-power/

73Gabriel Silan, J., Xu, S., & Apanada, M. J. (2024, May 23). Dual harvest: Agrivoltaics boost food and energy production in Asia. Insights. World Resources Institute. https://www.wri.org/insights/agrivoltaics-energy-food-production-asia

75Jamil, U. & Pearce, J. M. (2026). Agrivoltaics as a systems innovation: Multi-dimensional benefits from global studies across climate, agriculture, energy, and ecosystems. Renewable and Sustainable Energy Reviews, 230, 116721. https://doi.org/10.1016/j.rser.2026.116721

76School of Renewable Energy and Smart Grid Technology, Naresuan University. (2024). A Study on the Recommended Policies and Regulations Pertaining to Agrivoltaics in Thailand. https://caseforsea.org/post_knowledge/a-study-on-the-recommended-policies-and-regulations-pertaining-to-agrivoltaics-in-thailand/